Degas, 1873, Le Bureau du coton a la Nouvelle-Orleans

Suppose we have some quantity of good A on hand, and we will trade it for a suitable quantity of good B. We have a prior notion of the values of A and B by some knowledge of the world or levels of our inventories or our costs or other experience.

Notation:

a = The quantity of A that I offer for trade.

La = prior notion of value of A, expressed as units of essential value per unit of A.

Lb = prior notion of value of B, expressed as units of essential value per unit of B.

P(L) = Lb/La, the “natural” or “fair” price without profit.

b = The quantity of B that I want to receive in trade for a.

r = the rate of profit (or margin) that I intend to realize on the trade, expressed as a fractional increment of a.

p(r,{A,B}) = the price at which I receive a unit of B, that is, the number of units of A per unit of B, given a profit r. p(r,{A,B}) = p(r) if no ambiguity results.

Identities:

La * a = Lb * b for a trade without profit.

La * a * (1+r) = Lb * b for a trade with nonzero profit.

UBSS, the Unconditional Business Subsidy System, is a new concept (assembled from a few old ones), and now is an ideal time to establish it.

UBSS is an opportunity for Republicans and Democrats to forge an agreement for economic stabilization. It is simple in design, it subsidizes businesses, it maintains fiscal discipline, and it helps the people who need it the most.

UBSS makes an opportunity to resolve the discussion of the $600 per week emergency unemployment benefits boost. We can remove the $600 boost and replace it with UBSS.

Consider for a moment the existing system. We may suppose the prevailing view of economic stimulus tax cuts, grants and loans to business is that these are methods of improving the prosperity of the people. That’s not entirely false, but studies (for example, Gale and Samwick) show that the owners of the businesses enjoy 75% or more of the stimulative benefit, with the rest distributed to employees. In the existing system, the owners of the businesses get most of the money, not the employees, and not the general public.

In the existing system, despite stimulus, prosperity doesn’t improve. Our existing economic system supplies goods and services passably well to around 80% of the people. That’s quite a good accomplishment, but nevertheless, 15% live at the edge of personal financial disaster, and perhaps 5% often go to bed hungry, if they can find a bed.

In the existing system, tens of millions of people don't prosper, which limits the prosperity of businesses and their owners. Prosperous customers make prosperous businesses.

We need an improved approach.

Here is the idea of UBSS:

UBSS systematically connects the subsidy for businesses with new government revenue, so that the money paid out in business subsidies is systematically recaptured in taxes, giving it budgetary neutrality without risk of inflation.

UBSS subsidizes businesses via their customers. Each woman, man and child who resided in the United States the entire previous calendar year receives a uniform and equal payment each month, deposited by the Federal Reserve System (on behalf of the Treasury) in each person’s checking account (established, if necessary, for the purpose of receiving UBSS deposits). Each person chooses without constraint how to spend the money, generating transactions for businesses. The many transactions will subsidize all businesses and genuinely create jobs to supply the goods and services to these customers. The owners of businesses will be entitled to a fair profit from these transactions with customers.

Prafcke, “Automatic warehouse for small parts” (2003)

The aggregate distribution of subsidies in the current year can be known with high accuracy as the number of people multiplied by the uniform equal amount of the individual payment. In the current calendar year (2020), we collect the revenue based on incomes in the previous calendar year (2019), and we know with high accuracy the revenue collected on income in the second calendar year previous (2018).

For the current tax year, we can calculate a surtax on the largest ten percent of taxable incomes. The total surtax is the total population, multiplied by the uniform equal individual payment per month, multiplied by 12 months, less a compensating adjustment for the difference in surtax collected and the subsidies paid in the second year previous. To the largest one percent of taxable incomes, UBSS assigns two-thirds of the surtax. To the next largest nine percent of taxable incomes, UBSS assigns one-third of the surtax. The IRS will express the surtax as a percentage of taxable income.

Let’s consider specific numbers for UBSS. I suggest the uniform equal amount of $250 per month for each woman, child and man in the United States, indexed to the larger of the change in CPI and the change in income of the largest one percent of incomes. Here are some estimates.

Assuming the uniform equal amount of $250/month per person...

$990b/year = 330m population * $250/month * 12 months

$660b = two thirds of $990b

$2,500b = aggregate of the largest one percent of taxable incomes

26% = UBBS surtax rate on the largest one percent of taxable incomes

$330b = one third of $990b

$2,500b = aggregate of the next nine percent of taxable incomes

13% = UBBS surtax rate on the next nine percent of taxable incomes

Alternate assumption of the uniform equal amount of $125/month per person...

$495b/year = 330m population * $125/month * 12 months

$330b = two thirds of $495b

$2,500b = aggregate of the largest one percent of taxable incomes

13% = UBBS surtax rate on the largest one percent of taxable incomes

$165b = one third of $990b

$2,500b = aggregate of the next nine percent of taxable incomes

7% = UBBS surtax rate on the next nine percent of taxable incomes

I'm grateful for the work of Scott Santens for inspiration and for ideas contained herein, and to Dr. Linda Cunningham for suggestions and editing.

Aristocracy -- a.k.a. the One Percent. The wealthiest 1% of the people. No one is wealthier than the Aristocracy. Some Aristocrats work and some don’t. On average, about half their income arises from their Capital, that is, the things they own and their investments in businesses, stocks and loans and their claims on the Labor of others. Their own Labor produces the other half of Aristocratic income.

Board of Directors -- See Corporation.

Business School Professors -- Also known simply as the Professors, they study the FTC and the Economists and the Old Ones and sing the Tales. Professors love an audience. They will sing for anyone who wants to listen. Most often, however, they sing to instruct aspiring Professors, Economists and the Staffs in the characters and dynamics of the FTC.

Buyer -- In our advanced era, a trade typically involves money offered in exchange for a good or a service. In these money trades, we call the the two participants the Buyer and the Seller. The Buyer gives money to the Seller, and the Seller gives something to the Buyer.

Capital -- “Capital” has multiple meanings. It starts as something of value, usually money in a purse. The owner of the purse and money exchanges some of the money for Land, buildings and equipment, known as “fixed Capital” to the Old One Ricardo and the Professors, and exchanges some of the money for the wages of workers, tools, materials and supplies, known as “circulating Capital” to Ricardo and “working Capital” or "current assets" (depending on context) to the Professors. The workers combine the fixed and working Capital with their Labor, transforming the Labor and Capital into goods and services the owner sells at a higher value, called the surplus, than the combined costs of Labor and Capital from which the goods and services were produced. From the proceeds of the sale, the owner pays the costs of Labor and replaces the expended Capital, and adds the surplus to the ending Capital in the purse. In FTC, Labor has no claim on the surplus, which wouldn’t exist without the combination of both Labor and Capital. The surplus increments Capital, the property of the owner.

Capitalism -- The process by which the owner of Capital (the “Capitalist”), dependent on the defense of private property, invests owned Capital in expectation of replacing the invested Capital and receiving the surplus as an increment of owned Capital. Until 1848, the process had been described by the Old Ones Smith and Ricardo, and it was widely regarded as the unremarkable, undifferentiated natural condition of humanity. As a tree may divide into two branches, a differentiation attended the publication of the “Communist Manifesto”, by the Old Ones Engels and Marx, which called for the abolition of private property. Few words ever so nearly resembled a thunderbolt. After the “Manifesto”, there existed both “Communism”, which was a splinter of Socialism, and “Capitalism” which described both (a) the Capital-Labor-Capital transformation process and (b) the political anti-Communism movement. Marx himself used “Capitalism” on pages 307 and 314, in a chapter on the conversion of surplus value into Capital, of his little-read book “Capital” as a synonym of what he called the “capitalist system”. However, the word “Capitalism” didn’t enter common parlance until 1900. Capitalist -- See Capitalism and Socialism. Capitalist's Fallacy -- See Socialism. Capitalist of View -- See Socialism and Downward Trickle.

CEO -- See Chief Executive Officer.

Chairman -- We could refer to this person as the Chairwoman or Chairperson or Chair. In our enlightened modern age, however, the Chairperson is still, quaintly and almost always, a man. The Chairperson presides over the Board of Directors. See Corporation.

Chief Executive Officer or CEO -- a.k.a. President, the CEO is the manager who outranks all other Managers and Workers in a Firm. The CEO works to improve the Shareholders’ part of GDP10, and incidentally the CEO’s part of GDP10.

Conflict of Interest -- “A preposterously unlikely scenario in which the employee of a financial firm who could earn ungodly amounts of money by acting against a client's best interest might proceed to do exactly that. Conflicts of interest are pervasive, if not universal, on Wall Street.” (Zweig, 2015)

Corporation -- In 1600, Elizabeth I of England chartered the first Corporation, the East India Company. A Corporation is a collaboration among Shareholders, each Shareholder possessing one or more Shares. Each Share is a receipt for money contributed to the Corporation, showing the holder is a fractional owner of the Corporation. Each Share has equal value and one vote in matters of concern to the owners. The Shareholders appoint a committee, called the Board of Directors, of their number to oversee the activities of the Corporation. The Board of Directors choose the principal officers of the Corporation. The Corporation resembles a person, because it can autonomously conclude contracts, trade, incur debt, declare bankruptcy, and contribute to political campaigns. If the Corporation can’t pay its debts or fulfill contracts, then by law the Shareholders aren’t responsible.

The Curve of Laffer (artist's reconstruction) 2020

Curve of Laffer -- An ingenious explanation of the relationship between income taxes, the growth of GDP and the magnitude of government revenues. During the time of Reagan, the Economist Arthur Betz Laffer sketched the graphic Curve of Laffer on a paper napkin during a lunch with Dick Cheney and Donald Rumsfeld. Rumsfeld claims to retain the original in his private collection. The Curve shows that if the rate of taxation is zero, then government revenues are zero, because there is no tax, and if the rate is 100%, then government revenues are zero or nearly zero, because nobody wants to observably produce income, because the government would take it all. But if the tax rate is somewhere in between, then people have incentive to make more money, because high taxes don’t disincentivize them. Government revenues are higher, and there is some tax rate, not too low like point A on the graph, and not too high like point B, which maximizes government revenues. So, from point B on the graph, government revenues would increase if the tax rate was decreased! The increase in revenues would eliminate the fiscal deficit and reduce the national debt. Fully incentivized businesses would prosper, and the Downward Trickle would distribute the prosperity to everyone. Cheney, Rumsfeld and Laffer went to Reagan, the leader of their political party, the Tea Party, then known as the GOP. They showed Reagan the graph, and persuaded him the Sweet Spot was probably about 5%. In accordance with the Curve of Laffer, Reagan worked to reduce the top marginal income tax rate. The principal opposition party, the Dems, reluctantly accepted the lower tax. Revenues didn’t increase. They fell. National debt and fiscal deficit increased. Businesses did undertake some marginal projects they wouldn’t have ventured at a higher rate. GDP accelerated for about a year. On Black Monday, October 19, 1987, the prices of stocks on the Exchange crashed, and GDP subsequently declined. After Reagan, the Great Wars ended. The fiscal deficit continued, aggravated by a new war in Iraq. With chagrin, the Tea Party, that is, the GOP, raised the tax rate. GDP remained sluggish. Unemployment was a problem. The Dems gained dominance and raised the tax rate. Resulting budget surpluses suggested the Sweet Spot was probably greater than 30%. GDP rose. Unemployment fell. National debt fell. The Tea Party, still known as the GOP, regained power and reduced the tax rate, in accordance with the Curve of Laffer, to increase government revenues, and invaded Afghanistan and Iraq, and the fiscal surplus became deficit, and the prices on the Exchange crashed in the DotCom Crash of October 9, 2002, followed by higher unemployment and sluggish growth of GDP. The prices on the Exchange peaked on October 9, 2007, and began a slow decline.

A financial crisis ensued. Journalist Rick Santelli of CNBC revived the old name Tea Party in February 2008. Exchange prices hit bottom on March 9, 2009, about 6 weeks after the Dems took power. The Great Recession ensued. Unemployment was extensive in 2009, but it improved slowly. GDP grew, throughout the time of the Dems. Dem political power wasn’t sufficient to raise the tax rate until 2012 when the rate increased to 40%. With the continuing wars, deficits continued. GDP rose to record levels, Exchange prices rose to record levels, unemployment declined steadily. The Tea Party regained power, declaring themselves alternately the GOP and the Trump Party. In accordance with the Curve of Laffer, they reduced the income tax rate sharply for businesses in 2018. Unemployment continued to decline. GDP grew. Exchange prices rose to record highs, then tumbled in the Christmas Present MicroCrash of December 24, 2018. Exchange prices recovered over the next year to new highs, GDP grew, and unemployment declined to levels not seen since the late 1990s. Exchange prices fell about 40% in the Great Trump Crash of March 23, 2020, losing all the value gained since the Tea Party assumed power in 2017. Even in our enlightened modern era, you may hear from time to time a Professor or unintelligible Economist, sympathetic to the Tea Party, declare the Sweet Spot lies not at the current top marginal rate, nor at a higher top marginal rate, but at a lower top marginal tax rate, and that reducing the top marginal tax rate, in accordance with the Curve of Laffer, will produce a fiscal surplus, businesses will prosper, and the Downward Trickle will distribute the prosperity to everyone. The Dems, however, seem willing to agree the Sweet Spot lies somewhere around 55 to 65%.

Dotted line estimates the Sweet Spot.

Directors -- The Fairy Tale of Capitalism includes two meanings of “Director”. The first meaning is a level of Management. A Director is a Manager of Managers, though the Director usually isn’t an Executive. In the second meaning, a Director is a member of the Board of Directors that oversees the activities of a Corporation. Often, the Directors are nominated by the nominating committee of the Board of Directors. The shareholders elect the nominees because shareholders vote against the Board of Directors only in the most rare circumstances. The nominating committee, and the entire Board for that matter, are usually chosen from among the friends of the CEO, the Supercompensated CEOs of other Corporations, and from the spouses, children, nieces and nephews, siblings, and significant others of the Directors. See Corporation.

Ayn Rand, 1925

Downward Trickle -- The waste stream of the Aristocracy from which the 50 Percent may pluck a subsistence and an occasional boon. The Downward Trickle results from natural inefficiences in the Firehose Up. The Staffs work to improve the Firehose Up, which includes mitigating the Downward Trickle. The Old Ones knew of the Downward Trickle. Capitalists of View and Staffs often laud the Downward Trickle when seeking reduced taxes for the Aristocracy or less stringent regulation of their businesses. They say, as did Ayn Rand, that the Downward Trickle of Capitalism raises the standard of living of all people, which is why the inhabitants of slums in her era, the time of the Great Wars, lived like monarchs compared with ancient Egyptian slaves. Rand didn’t explain why slums exist and why children starve. See Firehose Up.

Economists -- Composers of Tales. Professors sometimes created tales, and sometimes other members of Society created tales, but Economists originated most of the Tales. The Old Ones wrote a few early Tales that became enduring classics.

Engels, Friedrich -- Sometimes called the “forgotten” Old One, Engels was Marx’s lifelong collaborator and source of financial support. His book “The Condition of the Working Class in England”, is an economic history describing the English industrial revolution in detail. It’s also a polemic, advocating for better treatment of Workers by their employers, the Ingenious Innovative Job Creators. Engels edited Marx’s grand work “Capital”, and may have contributed some sections. After Marx’s death, Engels completed the last volume of “Capital” from Marx’s notes. Engels remained an active Socialist until his death in 1895.

Exchange -- A big building housing a club of members who, acting on behalf of other persons for a fee, buy and sell shares of Firms “listed” on the Exchange. In our enlightened modern age, some members' fees charged to the general public have diminished to zero, a nice round figure popular with the public, and a "Free Lunch" in the argot of the Exchange, but that's another story. The Exchange is a Monop, de jure or de facto. If the Executives of a Firm wish to “go public”, that is, to sell shares of the Firm to the public, they deliver the shares to several of the members of the Exchange, and the members, for a fee, “list” the Firm and sell the shares to other members who, for a fee, buy the shares on behalf of persons in the general public. Sometimes Firm A acquires Firm B, in which case, Firm A buys all (or nearly all) of the shares of Firm B, and the Exchange “delists” shares of Firm B, and the members of the Exchange no longer buy and sell the shares of Firm B.

Executives -- A small subset of Managers, typically no more than a half-dozen per Firm. The Executives are the most highly ranking employees. They include persons with titles such as Chief Executive Officer (CEO), President, Chief Operating Officer (COO), Vice President, Chief Administrative Officer (CAO), Controller, Chief Technology Officer (CTO), Chief Financial Officer (CFO), Treasurer, and generally any Manager who reports directly to the President or CEO. The Executives have authority over all the other Managers of the Firm.

50 Percent -- The least wealthy half of the Society.

Firehose Up -- The Fairy Tale of Capitalism sometimes uses one term for multiple meanings. One meaning of "Firehose Up" refers to the more or less complex system of an Aristocratic household’s incomes from Capital (owned properties and wealth), Supercompensation, and all other income. A second meaning of “Firehose Up” is the modern system of complex conveyances transporting portions of GDP and the greater part of GDP growth to the Aristocrat, with legal authority maintained by the might of the government’s ships, soldiers and police. A third meaning of "Firehose Up" refers to all Aristocrats’ income sources as enabled and optimized by law, regulation, public policy, custom, convention and tradition.

See Downward Trickle.

Firms -- The Society organized itself into groups called Firms to find, gather, produce and distribute stuff.

Free Market -- In the Free Market, many buyers and many sellers compete. Any seller (or buyer), dissatisfied with a price (or product and price) offered by a buyer (or seller), can readily find another seller (or buyer) with whom to fairly trade. The Unfettered Free Market suffers from bandits, frauds and Monops who diminish competition, or defeat the buyers’ and sellers’ possession of the goods and services they trade, or defeat fair trades. Hence the Unfettered Free Market ceases to be a Free Market. Regulators, usually provided by Governments, inspect to assure safety and prevent abuses, and make rules to prevent harmful assymetries of information.

GDP -- See Gross Domestic Product.

Average Tax Rates (all taxes, divided by income) by Income Groups

Saez, Zucman "Progressive Wealth Taxation" (2019)

Government -- Government is the dominant coercive power in any region or other area of potential contention. Because government decides the prevailing law, government influences economic organization, taxes and regulation. The area of dominance of a government is its jurisdiction. The jurisdiction may be indistinctly defined. Government is inevitable, because always some one person or group of persons will have dominating coercive power. It’s not uncommon among the nation-states that the state security forces (military and police) will dominate, yet the security forces pledge loyalty, cede decision authority, and convey effective coercive power to a monarch, a dictator, a president, a prime minister or a parliament. In the case of “military Government” or martial law, the senior officer of the security forces decides the use of the dominant coercive power. Even in a region that has large, wealthy, well established institutions of government, a gang or militia may be the effective government, the dominant coercive force, in a neighborhood or subregion. Sometimes the region of a nation-state will have no powerful force authoritative throughout its territory. The militias of contending warlords divide the exercise of coercive power among themselves, such as Afghanistan at the times of the Soviet and American invasions, and Somalia at the time of the American invasion, and northern Europe during the era of the Roman Empire. American and European critics of such regimes sometimes call them “failed states”, a condescending term used to excuse invading the “failed state”. The mutual influence of the government and the economy, and the pertinent sphere of decisions, is often called Political Economy.

Average Tax Rates (all taxes, divided by income) by Income Groups

Saez, Zucman "Progressive Wealth Taxation" (2019)

Gross Domestic Product or GDP -- When a news announcer mentions the “Economy”, they most often refer to GDP in our modern enlightened age. Often unintelligible Economists speak of GDP as the fundamental measure of social well being. GDP is GNI Gross National Income plus some other stuff. GNI is the sum of all the incomes in a national subset of the Society. To get GDP, we can start with GNI, add the depreciation of capital equipment (usually about 16% of GDP in the USA), plus all the stuff sold to foreigners, minus all the stuff bought from foreigners (foreign transactions net about +/- 2% of GDP for large modern countries). Since the Ten Percent own nearly all the depreciating capital, the Aristocracy has a bit larger share of GDP than of GNI. Typically, all the news announcer knows about GDP is whether GDP is larger this quarter than the previous quarter (good news) or smaller (bad news). The Professors sing many versions of the perennial hit “Growth of GDP”. The Old One Adam Smith wrote the Tale of the Invisible Hand distributing income more or less evenly among the people, though he knew that Workers’ incomes were so small and unsteady that Workers sickened and starved during business cycles. In our modern enlightened era in the USA, the income of the Aristocracy is about 20% of GDP, the income of the Nine Percent is about 30% of GDP, and the income of the 90 Percent is about 50% of GDP.

“..., the top 10% income share is 50.5% in 2018, … . The top 1% income share increased from 20.7% in 2016 to 22.0% in 2017 and remained stable at 22.0% in 2018.” -- Emmanuel Saez, February 2020

Growth -- Usually implying growth of GDP. (Coincidentally, one of the most frequently covered songs of the Professors is “Growth of GDP”.) You may often hear the word “Growth” used as though it were a synonym of “Prosperity”, but it isn’t. See Prosperity.

Growth of Real Incomes -- Per the United States Census Bureau, household income in the United States in constant 2018 dollars was

in 1967

$ 47,085 for the 50th percentile (median)

$ 99,141 for the 90th percentile

$ 125,244 for the 95th percentile

in 2018

$ 63,179 for the 50th percentile $ 184,292 for the 90th percentile $ 248,728 for the 95th percentile

The increase from 1967 to 2018 was

34% for the 50th percentile

86% for the 90th percentile

98% for the 95th percentile

The ratio of the household income of the 95th percentile was

in 1967, 1.3 times the 90th, and 2.7 times the 50th in 2018, 1.3 times the 90th, and 3.9 times the 50th.

Income Disparity -- a.k.a. Income Inequality, describes large differences in incomes between the wealthiest people in the Society and the poorest people. The existence of dramatic Income Disparity corresponds with undemocratic dominance of the Government by the Aristocracy.

Income -- See Growth of Real Income

Income Inequality -- See Income Disparity.

Inequality -- See Income Disparity.

Ingenious Innovative Job Creators -- A term in FTC generally applied to Employers. But also, when the Staffs seek tax reductions for their Aristocrats, they present the Aristocrats as Ingenious Innovative Job Creators. In any case, the goal of reducing taxes almost always motivates those who use the term. Ingenious Innovative Job Creators need not be ingenious, nor innovative, nor need they create jobs. The key element of the term, of course, is “Job Creator”. Since a job is a transaction of work to be done in exchange for compensation, a job always involves two or more persons. Further, it’s not obvious that an employer actually creates a condition of work to be done, rather than recognizing a pre-existing condition which, perhaps, a Worker points out to them. In the case of the Aristocrat whose Staff seeks a tailored paragraph in the tax law, the Aristocrat may well be completely unaware of the condition. Workers, as the Old One Adam Smith knew, were often the first to recognize productive improvements, so the modifier “Ingenious Innovative” almost always properly applies to them, not to their employer. In FTC, the Workers are never called Job Creators, a term reserved only for the Capitalists possessing large amounts of money. Workers didn’t create jobs either, since they generally lacked the ability to compensate. Thus the term “Job Creator” is an absurdity.

Janissary Recruitment in the Balkans

Ali Amir Beg (ca. 1558), image: Wikimedia.org

Intellectual Property -- A government grant, to a person or Firm, of an exclusive monopoly on use of an idea. The right to use may be rented (via “royalties”) or sold to others by the owner of the Intellectual Property (IP). Ostensibly, IP compensates artists and scientists for bringing new ideas into the world. However, IP disincentivizes use of the idea, discourages new ideas the idea may inspire, contributes to monopoly practices, and creates an industry of lawyers and accountants who challenge or defend IP in court and oversee the collection of royalties.

Invisible Hand -- An articulation by Adam Smith of the notion that an individual, by pursuing their own interest, does thereby improve the Society. Usually taken out of context from a subtopic of a discussion of domestic versus foreign trade in Smith’s book “Wealth of Nations” (1776). That context sprawls across several paragraphs, which we abbreviate here, in Smith’s words:

But it is only for the sake of profit that any man employs a capital in the support of industry; … He generally, indeed, neither intends to promote the public interest, nor knows how much he is promoting it. … he intends only his own security; … he intends only his own gain; and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention. Nor is it always the worse for the society that it was no part of it. By pursuing his own interest, he frequently promotes that of the society more effectually than when he really intends to promote it.

Adam Smith

by John Kay (1790)

Marx, Karl -- Marx and his collaborator Friedrich Engels are two of the Old Ones. Their “Communist Manifesto”, which they wrote in 1848 on behalf of the Communist League (disbanded in 1852), clearly called for abolition of private property and overthrow of government, and less prominently advocated a graduated income tax, abolition of child labor, and free education in public schools. The Manifesto was printed in dozens of languages throughout the world. Also, they described in detail, and with scorn, what they called the “capitalist system” in their immensely influential economic treatise “Das Kapital”. Marx taught that the economic system of a society (the means of production) determines the political character of the society. Marx advocated for the superstition that communist revolution was scientific and inevitable. He lived and died in poverty. His grave is in a cemetery in Highgate, London, UK.

Labor -- As often seen in the FTC Fairy Tale of Capitalism, a word will have two meanings. “Labor” and “Worker” are synonyms. Also, “Labor” is the productive activity of the Workers. In the sense of activity, Labor transforms Capital into valuable and useful products. The wage, the cost of Labor, is the cost sufficient to get a Worker to show up for work next week, and relates rarely and temporarily to the value of the products. See Workers.

Labor Theory of Value -- One of the Tales of the Old One Ricardo. “In estimating the exchangeable value of stockings, for example, we shall find that their value, comparatively with other things, depends on the total quantity of labour necessary to manufacture them, and bring them to market.” (Ricardo, 1817)

David Ricardo

by Thomas Phillips (1821)

Land -- The Old Ones Adam Smith and, especially, David Ricardo, wrote of three indispensable factors of production: Labor, Capital, and Land. Ricardo gave much attention to the Rent a landlord can collect from their agricultural Land, which amount is determined by the value of crops grown on the land of poorest quality. If the poorest tilled land produces 10 tons per season per acre of tomatoes, then the value of those tomatoes is the cost of Labor to produce them, which is the cost of feeding the Labor sufficiently that they will show up for work during the next week, and the Rent available from this poorest Land is nothing but a ceremonial fee to acknowledge permission to farm and ownership. If the next poorest land produces 20 tons per season per acre of tomatoes, with the same Labor of cultivation, then the Rent on this next poorest Land is equal to zero (the value of the Rent on the poorest Land), plus the value of the additional production of 10 tons of tomatoes. If the best Land produces 50 tons per season per acre of tomatoes, with the same Labor of cultivation as the poorest Land, then the Rent on the best Land is equal to the value of 40 tons of tomatoes. The Professors often sing variations of Ricardo’s tales of the Labor theory of value and the value of Rents on Land. They remain key Tales of economics with numerous analogs in realms of thought far removed from agricultural Land, such as the value of obsolete computer equipment, even in our enlightened modern era.

Managers -- Managers oversee the planning and operation of Firms and the direction of workers. Owners may also Manage, if they wish, but Ownership doesn’t require it. The notion of Management originated early in the period of the Great Wars. From then until our enlightened modern era, four types of Manager have evolved: Supervisors (a.k.a. “Managers”), Directors, Executives and the Chief Executive Officer (CEO).

Monop -- A Monopoly or Monopsony, depending on context. See Monopoly. See Monopsony.

John D. Rockefeller (ca. 1875)

Monopoly -- A general economic condition in which buyers have no choice but to buy from a single seller. In pure form, which seldom occurs without government controls, there is exactly one seller. In free markets, if there are fewer than seven sellers, then usually, the economic effect is so similar to pure Monopoly that each of the sellers is considered a Monopoly. Or, if one seller sells more than 30% of the product in a market, then usually, that seller is, effectively, a Monopoly. If there is a Monopoly in some product or service, then no fair trade can exist, because a buyer gets no improvement in terms of trade by choosing another seller. See Monop. See Monopsony.

Monopsony -- A general economic condition in which sellers have no choice but to sell to a single buyer. In pure form, which seldom occurs without government controls, there is exactly one buyer. In free markets, if there are fewer than seven buyers, then usually each of the buyers is considered a Monopsony. Or, if one buyer buys more than 30% of the product in a market, then usually that seller is, effectively, a Monopsony. If there is a Monopsony in some product or service, then no fair trade can exist, because a seller gets no improvement in terms of trade by choosing another buyer. See Monop. See Monopoly.

Nine Percent -- The Nine Percent and the Aristocracy, considered together, are the Ten Percent of households that have higher incomes and greater wealth than anyone else in the Society. In the USA, the Nine Percent get roughly 30% of national aggregate household incomes. About 7% to 10% of their incomes arises from ownership of Capital and businesses, and most of their income arises from their Labor.

90 Percent -- The least wealthy 90% of the Society, that is, all of the Society except the Ten Percent. The 90 Percent includes most of the Workers and small business owners, and all of the poor people. Nearly all of their income arises from their Labor.

99 Percent -- All of the Society except the Aristocracy, that is, the 90 Percent and the Nine Percent, combined.

Occupy Wall Street -- A protest movement that began on September 17, 2011 in Zuccotti Park in New York City and spread from there throughout the world. OWS had no formal leadership and no clear agenda. Wikipedia attributes predecessor protests at the University of California in 2008, and Kalle Lasn of the Canadian group “Adbusters” as the initiator of the call for protest in New York. Extreme inequalities of wealth and incomes, greed, unfair influence of large corporations, and corruption in government were principal concerns. Observers of OWS often heard the slogan “We are the 99%”.

Old Ones -- The Old Ones wrote the most significant early Tales, in both small and immense volumes of unintelligible prose. The Old Ones were Adam Smith, David Ricardo, Karl Marx, and Friedrich Engels.

One Percent -- See Aristocracy.

OWS -- See Occupy Wall Street.

Piketty, Thomas -- An unintelligible Economist of our enlightened modern age and author of the intensively researched book “Capital in the Twenty-First Century” and the subsequent “Capital and Ideology”. Dr. Piketty’s writings provide the most detailed information on the inequality of incomes and wealth from times before the Old Ones to the present.

Potential Conflict of Interest -- “An actual conflict of interest.” (Zweig, 2015)

Professors -- See Business School Professors.

Prosperity -- Thriving with comforts and happiness. Not a synonym for “Growth”. See Growth.

Rand, Ayn -- Rand escaped from Stalinist Russia and took refuge in New York City, where she established an anti-communist intellectual salon. She advocated for the superstition that virtuous selfishness is objective and rational. She wrote a lucid defense of capitalism in her book “Virtue of Selfishness”. Her books remain widely read in our modern enlightened era, including “Fountainhead”, “Atlas Shrugged”, and others.

Real Incomes -- See Growth of Real Incomes.

Portrait of Ricardo

by Phillips (1821)

Ricardo, David -- The Old One Ricardo acquired great wealth trading shares on the Exchange. He wrote the treatise “On the Principles of Political Economy and Taxation” (1821), expostulating precise and enduring economic theories. Among these was the profound, but hardly obvious, “Tale of Comparative Advantage”, in which he showed that two countries, with their Workers unable to travel between them, could maximize their aggregate incomes if each concentrated their Workers’ efforts on making those products which they were best able to produce, selling what excess they couldn’t use to inhabitants of the other country. Economists of our modern enlightened era labeled another tale "Ricardian Equivalence", which implies that a stimulative government subsidy doesn't save, because the people save the money received, which more or less describes the behavior of the Aristocracy, the usual recipients. Ricardo also explained that the natural level of Workers’ wages is the price that enables the Workers to subsist.

Sachs, Jeffrey -- A Professor and, oddly, a relatively intelligible Economist of our enlightened modern era. Dr. Sachs advocates collaborative relationships between governments and privately owned organizations. During the late 1900s, Sachs advised new governments, including the government of Russia, that emerged when the Soviet Union ended. He advises the Secretary-General of the United Nations.

Saez, Emmanuel -- An unintelligible research Economist, Director of the Center for Equitable Growth at the University of California in Berkeley, and a collaborator with Piketty and Zucman. Economists hold Saez in high regard for the arcane mathematical runes with which he always punctuates his expressions. Saez also has talent for pictures, unusual among Economists.

Shareholders -- See Corporation. Synonym: Stockholders.

Smith, Adam -- The earliest of the four Old Ones. Often remembered for his Tale of the Invisible Hand. Smith also articulated the principles of division of labor and of the wealth enhancements through technological innovation. Some Capitalists of View may be heard to assert that Smith was a capitalist, which he was not. However, Smith described the economic system of his time, which was in his day accepted as the only economic system, a natural condition, and the default condition if the state protects private property and doesn’t participate in distributing wealth or income. Smith wrote that workers compete, bidding against one another for employment, which competition keeps their wages to a “scanty subsistence”.

Socialism -- An amorphous social and political movement, historically manifested in various forms, clustered around the concept that all persons have the right to a sustaining share of the political participation and economic benefits of the general Society. Socialism has no primary leader who dictates the principles and beliefs of Socialism. An early organized form was Chartism in the 1800s, a rallying of Workers around the People’s Charter of 1838, a list of six democratic political reforms, including universal male suffrage and secret ballots. Closely associated with labor unions, Chartists organized some of the earliest strikes of workers against their employers, seeking higher wages and improved working conditions among other things. Early Socialism included benevolent organizations providing housing for workers and communally owned businesses. From Socialism emerged the concepts of universal public education, the graduated income tax, and abolition of child labor. The “Communist League” was an organized political splinter party that commissioned the Old Ones Engels and Marx to write the party’s program in 1847, which was published as the “Communist Manifesto” in 1848. The League was formally dissolved by the remaining members in 1852. Nearly all of the Communist League would have regarded themselves as Socialists. Twentieth century autocrats including Stalin, Mao and some autocrats of our enlightened modern era have called themselves Communists. Some Capitalists of View assert with invalid inference that Socialism is or leads to autocracy. Stalin was an autocrat, Stalin was a Communist, Communists are Socialists, so Socialists are autocrats, which is the Capitalist’s Fallacy. Some Capitalists of View assert that Capitalism is or leads to personal freedom, despite the numerous counterexamples including Hitler's Germany, Pinochet's Chile, Franco's Spain, the Atlantic slave trade, 21st century China, Ernesto Geisel's Brazil, Duvalier's Haiti, Videla's Argentina

Society -- All of the people, the Aristocrats, the Nine Percent, the 90 Percent, everyone. The Society organized itself into groups called Firms to find, gather, produce and distribute stuff.

The Denmark Staff, Maersk Lines, 1914, shared per license

Staff -- Aristocrats and their families have Staffs. A Staff is one or more people, including accountants, lawyers, financial experts, lobbyists, administrators and others, who supervise the household finances and the owned businesses of the Aristocrats. Staffs report regularly to their principals on their after-tax income during the latest quarter ended, and they hope always to be able to report some increase in income from the prior period. The Aristocrat may know little about managing money or running a business, but they understand the significance of increasing or decreasing income. Staffers who report the Aristocrat’s family’s income increasing reliably from quarter to quarter will likely enjoy increases in their own incomes. Staffers who report income declining from quarter to quarter may not remain in the employ of the Aristocrat the following year. Staffers always seek to reduce their employer’s tax burden, because reduced taxes increase an Aristocrat’s income. They seek to reduce or eliminate government regulations that interfere with the Aristocrat’s businesses’ opportunities to profit by increasing the businesses’ revenues or by reducing the incomes of suppliers, workers and customers or by exploiting a public resource. For the same purpose, the Staff work to persuade legislators and regulators to create special amendments to laws and regulations that favor the income of their Aristocrat. The aggregate efforts of all the Staffs of all the Aristocrats maintain and intensify the inequality of incomes in the Society. The Staffs produce inequality of incomes.

Stiglitz, Joseph -- After the Great Wars, the unintelligible Economist Dr. Joseph Stiglitz received high awards and wrote many widely read books on assymetrical information (where parties to a trade have differing knowledge of the character of the goods exchanged) and on the economic costs of extreme inequality of incomes.

Stockholders -- See Shareholders.

Supercompensation -- Money that Firms pay to their CEOs far in excess of the money paid to other employees of the Firm, far in excess of the value they produce for the company, and far in excess of the value of a human life. In our enlightened modern era, not infrequently, the CEO (or other highly-compensated employee) will receive pay more than 160 times the value of the median amount of money paid to individual employees. In the United States, if the typical Worker does excellent work every year and so earns substantial wage raises every year for 50 years, then the Worker will have approximately the same level of pay as the typical CEO.

Supervisors -- Managers who manage Workers directly.

Tales -- See Old Ones.

Boston Tea Party by Cooper (1789, USA Public Domain)

Tea Party -- An old political party for Capitalists of View. The primary policy objective for hundreds of years has been to increase the net income (after taxes) of the Aristocracy during the next two or three years. All other policies are subordinate, less important, reversible, and generally adopted or opposed or ignored at one time or another for expediency. Most of the Staffs prefer the Tea Party, though Aristocrats don’t necessarily. The Tea Party, also called at times the GOP and the Trump Party, flourished during the time of Reagan, then faded, revived with vigor in February 2008, and persists in our enlightened era. See also Curve of Laffer.

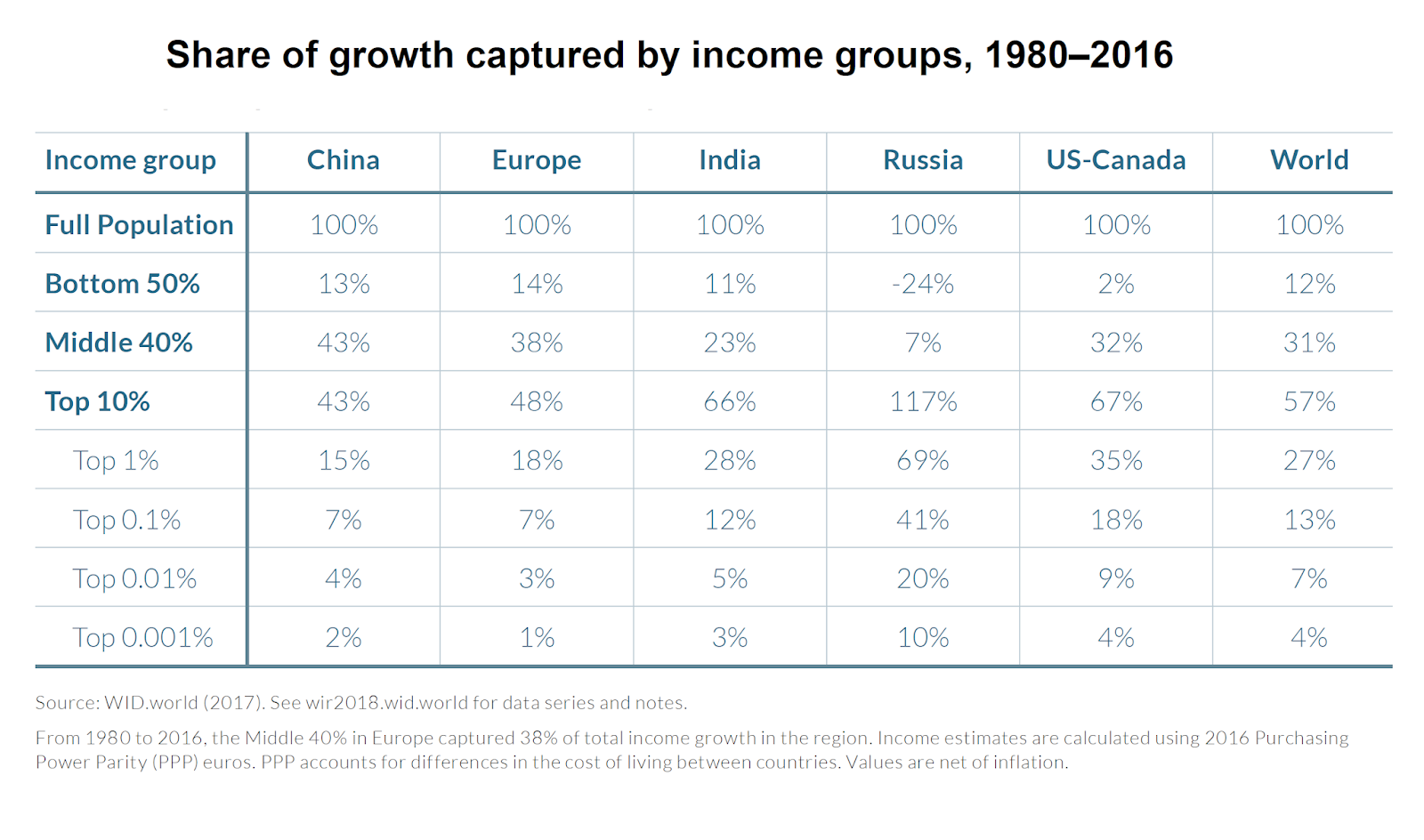

In the US, the Ten Percent collect about 2/3 of total income growth,

and the 40 Percent capture nearly all of the rest.

Ten Percent -- The wealthiest tenth of the population of the Society. The Old Ones Marx and Engels called this tenth the Bourgeoisie, and referred to them as the owners of Capital.

Trade -- In a trade, there is always at least one buyer and one seller. These are the parties to the trade. Each of the parties gives up something they want less in exchange for something they want more. Each party benefits from the trade. The benefit is the difference between the thing wanted more and the thing wanted less, a kind of profit for each party. Each party has a choice whether to participate in the trade. Each party may decline to participate. Each party may choose some other person with whom to trade. Usually, the buyer is the party who gives up cash, and the seller is the other party. If both parties have a wide range of counterparties from whom to choose, and if they both participate freely, without coercion or deception, then we call it a fair trade.

Transaction -- Synonym of Trade.

Unemployment -- The Old One Engels noted in his “The Condition of the Working Class in England” that the factories would build up their operation, sometimes at a high tempo, and continue producing for six to ten years. Then a waning of revenues would affect most of them more or less simultaneously so that the product of a factory working at capacity couldn’t be sold at a price sufficient to pay the costs. Among these costs was the wages of the workers, since the workers weren’t considered legally interested in the ownership and profits. Simply reducing the wages did not go well with the workers. For the better paid workers, their pride suffered, and they felt unjustly rewarded for their efforts, kindling resentments and animosity. But for most workers, since their wages just barely sufficed to feed their families for a few more days, a reduction in wages implied insufficient food to sustain them, and some of them would become desperate and unpredictable. The level of wages, like all other choices in the Firm, were the decision of the managers, the executives, the board of directors, the Staffs, the Ingenious Innovative Job Creators, and ultimately the Owners. Given the adverse effects of reducing wages, the Ingenious Innovative Job Creators typically chose to dismiss some of the Workers so that the number of remaining Workers corresponded with the level of production. “Dismiss” meant discontinuing the employment and the wages. The people of the general Society described the dismissed Worker as “unemployed” and existing in a state of “unemployment”. Since multiple factories in the region would dismiss Workers at about the same time, the Workers contended with each other. Few Workers could find quickly a new job and a new stream of wages. Since they didn’t participate in the profits of the Firms, and since their wages had dropped to zero, “unemployment” meant “starvation”.

Wealth -- Wealth has multiple meanings in the Fairy Tale of Capitalism. Most often, Wealth refers to a kind of property capable of becoming the Capital component in the transformation of Capital by Labor into product exchanged for incrementally larger Capital for the owner. More than half the income of the Aristocracy consists of the increments this kind of Wealth produces. Another usage of “Wealth”, usually in the adjectival form “Wealthy”, pertains to a person with a relatively large income, especially when that income is Supercompensation. The Aristocracy are always considered Wealthy. Not uncommonly, the Ten Percent are considered Wealthy, depending on the context. The 90 Percent are never considered Wealthy. The unintelligible economists Chetty and Hendren found that children of households in less wealthy neighborhoods that move

Albert Parsons, leader of a railway strike in 1877

to wealthier neighborhoods become wealthier adults than children of households in less wealthy neighborhoods that don’t move.

Workers -- People for whom nearly their entire income arises from compensation for their Labor. Labor is the productive activity of the Workers. Nearly all of the 90 Percent are Workers or dependents of Workers. Most of the Ten Percent are Workers, too, though they tend to derive some income from their property. See Wealth. See Labor.

Working Class -- See Workers.

The Staffs told their children that the Old Ones Karl Marx and Friedrich Engels were the bad guys, and Adam Smith and David Ricardo were the good guys.

Unless I'm mistaken, this Encyclopedic Glossary is the (chronologically) last chapter of the Fairy Tale of Capitalism.

I will always have deep gratitude for the prepublication reviews, the editing, the advice and the encouragement of friends and associates. While I prefer think of all of them as significant, I must mention explicitly the kind help and interest of Mr. Don Zirulnik, Dr. Doug Stetson, Mr. Richard Leaf, Mr. John Brockman, Ms. Nancy Flack, Dr. James Reeves, Dr. Dennis Martin, and especially Dr. Linda Cunningham.

Images

All images are either in the Public Domain or used as allowed under Fair Use doctrine.

Raj Chetty, Nathaniel Hendren, “The Impacts of Neighborhoods on the Intergenerational Mobility I: Childhood Exposure Effects” (Quarterly Journal of Economics, Feb 10, 2018, https://doi.org/10.1093/qje/qjy007)

Raj Chetty, Nathaniel Hendren, “The Impacts of Neighborhoods on the Intergenerational Mobility II: County-Level Estimates” (Quarterly Journal of Economics, Feb 10, 2018, https://doi.org/10.1093/qje/qjy006)

Raj Chetty, Nathaniel Hendren, Patrick Kline, Emmanuel Saez, “Where is the land of Opportunity? The Geography of Intergenerational Mobility in the United States” (Quarterly Journal of Economics, Sep 14, 2014, https://doi.org/10.1093/qje/qju022)

Friedrich Engels, “The Condition of the Working Class in England” (1845, http://amzn.to/2snelK9)

Thomas Piketty, “Capital and Ideology” (2020, https://www.amazon.com/dp/0674980824)

Thomas Piketty, “Capital in the Twenty-First Century” (2017, https://www.amazon.com/dp/0674979850/)

David Ricardo, “On the Principles of Political Economy and Taxation” (1817, 1821) http://www.econlib.org/library/Ricardo/ricP.html

Emmanuel Saez, “Striking it Richer: The Evolution of Top Incomes in the United States (Feb 2020, UC Berkeley, https://emlab.berkeley.edu/~saez/saez-UStopincomes-2018.pdf)

{kind=link}

{kind=link}

{kind=link}

_(7312784848).jpg){kind=link}

{kind=link}

{kind=link}